Financial Fraud Investigations: Connecting the Evidence

Fraud rarely begins when it is discovered. By the time suspicious transactions, compliance alerts, or internal audits bring attention to a case, the activity may have been occurring for months or longer. According to the ACFE's 2024 Report to the Nations, organizations lose an estimated 5% of annual revenue to occupational fraud, and the median scheme runs for twelve months before detection. The challenge is not simply identifying that something suspicious happened. It is understanding what happened, who was involved, and how much damage occurred before anyone noticed.

In this article, we examine what financial fraud investigation looks like today, why modern fraud has become more difficult to investigate, how investigators build cases from multiple forms of evidence, and where OSINT and AI are changing the investigative process.

A financial fraud investigation is the process of determining whether fraudulent activity occurred, identifying the people and entities involved, tracing how the activity took place, and gathering evidence that supports legal, regulatory, disciplinary, or recovery actions.

Historically, financial fraud investigations were heavily associated with forensic accounting. Investigators reviewed financial records, reconciled transactions, identified discrepancies, and followed money through accounting systems. Those activities remain important, but they no longer represent the full scope of modern investigations.

Today, investigators routinely work across financial records and transaction data, corporate ownership information, digital communications, identity records, device and access logs, cryptocurrency transactions, public records, open-source intelligence, and adverse media reporting. The scope has expanded because the fraud landscape has expanded.

The distinction between detection and investigation is worth making explicit. Detection identifies anomalies: a transaction monitoring system flags unusual payments, an AML platform generates an alert, a compliance review surfaces inconsistencies. Investigation answers what follows. Why did the anomaly occur? Who was involved? Was the activity intentional? Are multiple entities connected? Is the behavior part of a broader scheme? Detection surfaces a signal. Investigation builds a case.

Financial fraud has evolved alongside the systems it targets. Corporate ownership structures can span multiple jurisdictions and layers of holding companies. Digital services allow accounts, infrastructure, and communications to be created rapidly and abandoned just as quickly. Cryptocurrency introduces transaction environments that may sit entirely outside traditional banking records. Synthetic identities combine real and fabricated information to create convincing personas that pass basic verification checks.

AI has introduced another layer of complexity. Fraudsters now use AI-generated documents, synthetic profile images, deepfake audio, and automated communication systems to scale fraud operations while making attribution more difficult. What once required substantial effort and resources can now be generated at volume with minimal technical skill.

The result is an environment where the evidence needed to understand a fraud scheme is fragmented across financial systems, digital platforms, corporate records, and public sources. Investigators may need to connect financial activity, corporate records, identity information, communication patterns, digital infrastructure, public reporting, and behavioral indicators across systems that were never designed to integrate with each other.

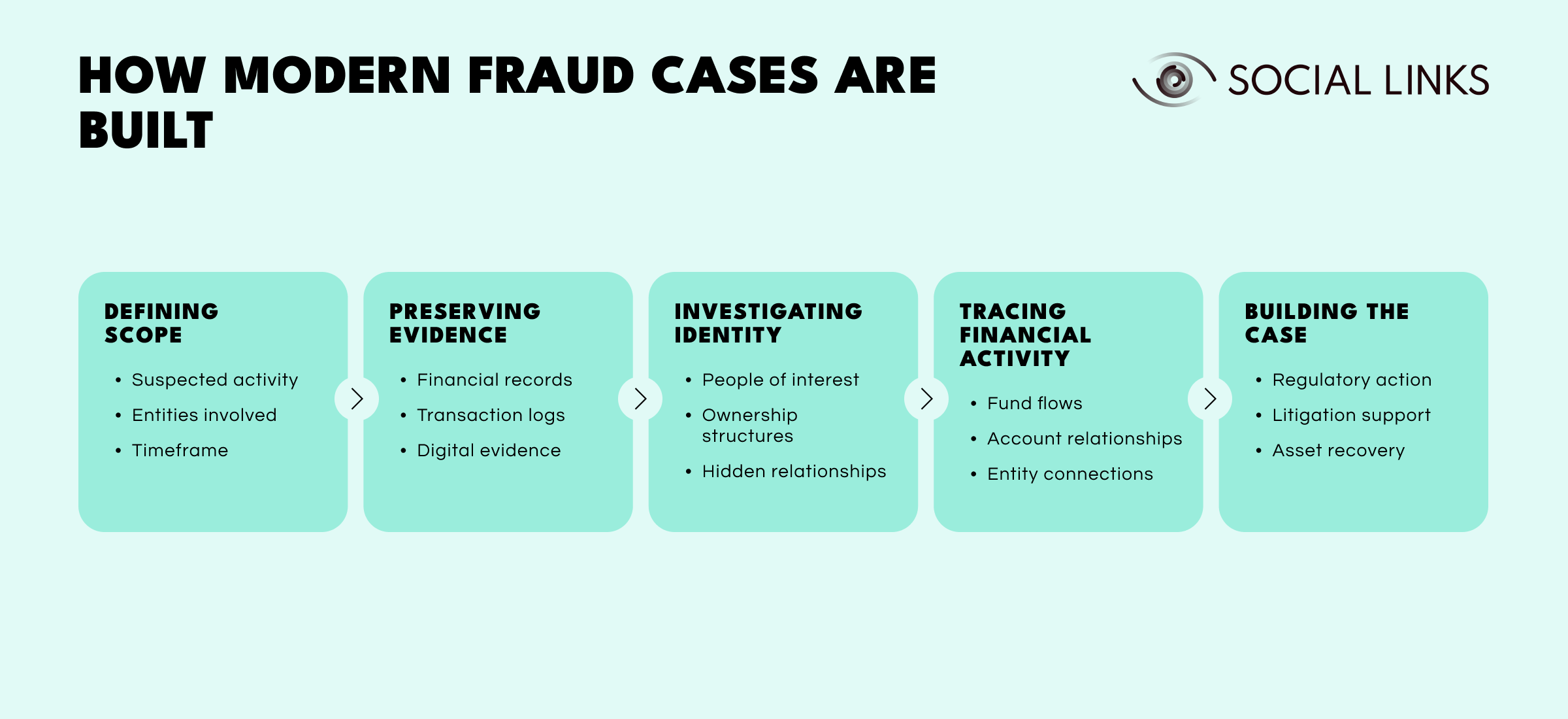

Every case is different, but most financial fraud investigations follow a similar logical sequence.

Defining scope. Investigations begin by identifying the suspected activity, the entities involved, the time period under review, and the potential impact. At this stage the goal is not to prove fraud immediately but to establish the boundaries of the inquiry and determine what questions need to be answered.

Preserving evidence. Once an investigation begins, evidence must be collected and preserved in a manner that maintains integrity and supports future review. Financial records, communications, transaction logs, documents, and digital artifacts may all become relevant. Early preservation matters because evidence can be altered, deleted, overwritten, or lost over time.

Investigating identity. Modern fraud cases frequently involve unknown counterparties, intermediaries, beneficial owners, or synthetic identities. Investigators examine individuals, organizations, and relationships to understand who is actually behind the activity and whether declared identities match observable reality. The ACFE's 2024 Report found that 84% of fraudsters exhibited behavioral red flags before detection, underscoring why understanding the individuals behind a scheme is often as important as tracing the transactions themselves.

Tracing financial activity. The financial component focuses on tracing funds, identifying movement patterns, mapping relationships between accounts, and understanding how assets entered, moved through, and exited a scheme. This step often reveals connections that are not immediately visible from isolated transactions.

Building the case. The final objective is not simply collecting information. Findings must be organized into a coherent narrative supported by evidence. Whether the outcome involves regulatory reporting, litigation, internal disciplinary action, asset recovery, or criminal prosecution, the investigation must demonstrate what happened and why the conclusions are supported.

Financial records explain transactions. They do not always explain the people, entities, or relationships behind them. This is where open-source intelligence becomes valuable.

OSINT extends investigations beyond internal records and structured financial data by incorporating information from publicly available sources. Corporate registries, beneficial ownership records, court filings, regulatory disclosures, sanctions lists, public procurement databases, social media activity, adverse media reporting, and leaked breach data can all provide context that financial statements cannot.

Consider a transaction involving an unfamiliar vendor. Accounting records confirm that payments were made. Corporate filings may reveal ownership structures that connect to related parties. Adverse media may identify prior fraud allegations against the same individuals. Social media activity may show undisclosed relationships between executives and counterparties. Public procurement records may reveal patterns across multiple organizations.

Each source provides a fragment of the full picture. Together they create context. This investigative layer often becomes the connective tissue between suspicious financial activity and the individuals or organizations responsible for it, connecting what financial analysis surfaces to who is actually behind it.

AI is changing both fraud detection and fraud investigation, but not in the same way.

On the detection side, AI excels at identifying patterns across large datasets. Financial institutions increasingly use machine learning models to monitor transactions, detect anomalies, identify unusual behavior, prioritize alerts, and reduce false positives. These systems help surface activity that may warrant investigation.

The investigative layer is different. Here, AI is increasingly used to accelerate analysis rather than make conclusions. Entity resolution connects individuals and organizations across fragmented data sources and jurisdictions. Relationship mapping surfaces connections between entities that would take significant manual effort to identify. Document classification and data enrichment help investigators process larger volumes of information more quickly than manual review alone would allow.

Human judgment remains central throughout. AI can identify potential connections between entities but cannot reliably determine intent. It can highlight patterns but cannot independently assess credibility. It accelerates analysis but does not replace investigative reasoning. The strongest investigative programs treat AI as an amplifier for analysts rather than a substitute for them.

Successful investigations depend less on individual tools than on the ability to connect information across systems, disciplines, and teams.

One common failure occurs when fraud detection and fraud investigation operate as separate functions. Transaction monitoring teams generate alerts. Compliance teams review documentation. Fraud analysts examine activity. Investigators become involved later, often after evidence has become fragmented or difficult to reconstruct. Effective programs close that gap. Detection workflows should feed directly into investigative processes. Evidence should be preserved as soon as suspicious activity is identified. Financial records, digital evidence, identity information, and external intelligence should be evaluated together rather than in isolation.

Cross-functional coordination matters equally. Financial fraud investigations often involve compliance teams, fraud analysts, financial investigators, legal departments, risk teams, digital forensic specialists, and intelligence analysts simultaneously. Each group contributes a different perspective. Cases become stronger when those perspectives are connected rather than siloed.

The organizations that investigate fraud most effectively are not necessarily the ones with the largest investigative teams. They are the ones that create clear pathways between detection, investigation, evidence preservation, and decision-making.

Financial fraud investigation has evolved far beyond its traditional association with forensic accounting and transaction review. Modern investigations combine financial analysis, identity verification, digital evidence, open-source intelligence, and AI-assisted analytical workflows. Fraud schemes operate across multiple systems and jurisdictions, leaving evidence that is distributed rather than centralized.

Successful investigations depend on the ability to connect those layers into a coherent understanding of what happened, who was responsible, and what action should follow. Detection identifies suspicious activity. Investigation transforms that activity into evidence, context, and ultimately accountability.

A financial fraud investigation is the process of identifying, examining, and documenting fraudulent financial activity while collecting evidence that supports legal, regulatory, disciplinary, or recovery actions.

Forensic accounting focuses primarily on financial records and transactions. Modern financial fraud investigations combine forensic accounting with digital evidence, identity analysis, OSINT, and broader investigative techniques that extend beyond the accounting record.

OSINT helps investigators understand the people, entities, relationships, and external indicators that may not appear in internal financial records alone. Corporate registries, adverse media, social media, and public filings all provide context that financial statements cannot.

AI supports anomaly detection, entity resolution, relationship mapping, identity analysis, and large-scale data review. It accelerates analysis but does not replace human judgment, particularly in attribution, intent assessment, and case-building decisions.

Evidence can be altered, deleted, or lost over time. Early preservation maintains integrity, supports future review, and strengthens legal or regulatory outcomes. Investigations that begin preservation late frequently face gaps in the evidentiary record that weaken their conclusions.

Want to see how OSINT supports financial fraud investigations in practice? Book a personalized demo with one of our specialists and discover how SL Crimewall helps investigators connect financial activity, identity data, digital evidence, and external intelligence into a coherent evidentiary picture.