Due Diligence: A Higher Standard

Organizations routinely commit significant capital, enter long-term vendor relationships, and expand into new markets based on due diligence processes that have not fundamentally changed in decades. Questionnaires get completed. Documents get reviewed. Boxes get checked. The relationship proceeds. What rarely happens is a genuinely investigative examination of whether what an entity declares matches what independent inquiry reveals.

Regulatory expectations have hardened considerably across multiple frameworks simultaneously, extending due diligence obligations well beyond the transaction context into ongoing vendor relationships, supply chains, and ESG accountability. The standard most organizations apply has not kept pace.

In this article, we examine what due diligence actually involves today, how it has evolved from a compliance exercise into a multi-layered investigative function, what the regulatory environment now requires, and why the standard most organizations apply is no longer sufficient.

Due diligence is the process of investigating a person, organization, or opportunity before committing to a significant decision. In a business context, that means examining the financial, legal, operational, reputational, and relational dimensions of a potential partner, acquisition target, vendor, or counterparty to understand what is actually being committed to, not just what is being represented.

Due diligence as a business concept traces to the United States Securities Act of 1933. Under Section 11, underwriters and others involved in securities offerings could avoid personal liability for material misrepresentations by demonstrating they had conducted a reasonable investigation. That legal standard gave due diligence its early association with document review, financial verification, and compliance checking. What it now requires has expanded considerably beyond those origins.

The questions organizations need to answer have become significantly more complex. Who actually controls this entity? Who benefits from this transaction? What relationships exist that do not appear in the official ownership structure? Has this counterparty, its directors, or its beneficial owners been associated with regulatory action, sanctions exposure, or adverse media in any jurisdiction? What does observable evidence suggest about how this entity actually operates, as opposed to how it presents itself?

These are investigative questions, not compliance questions. Answering them requires methods that go well beyond document collection.

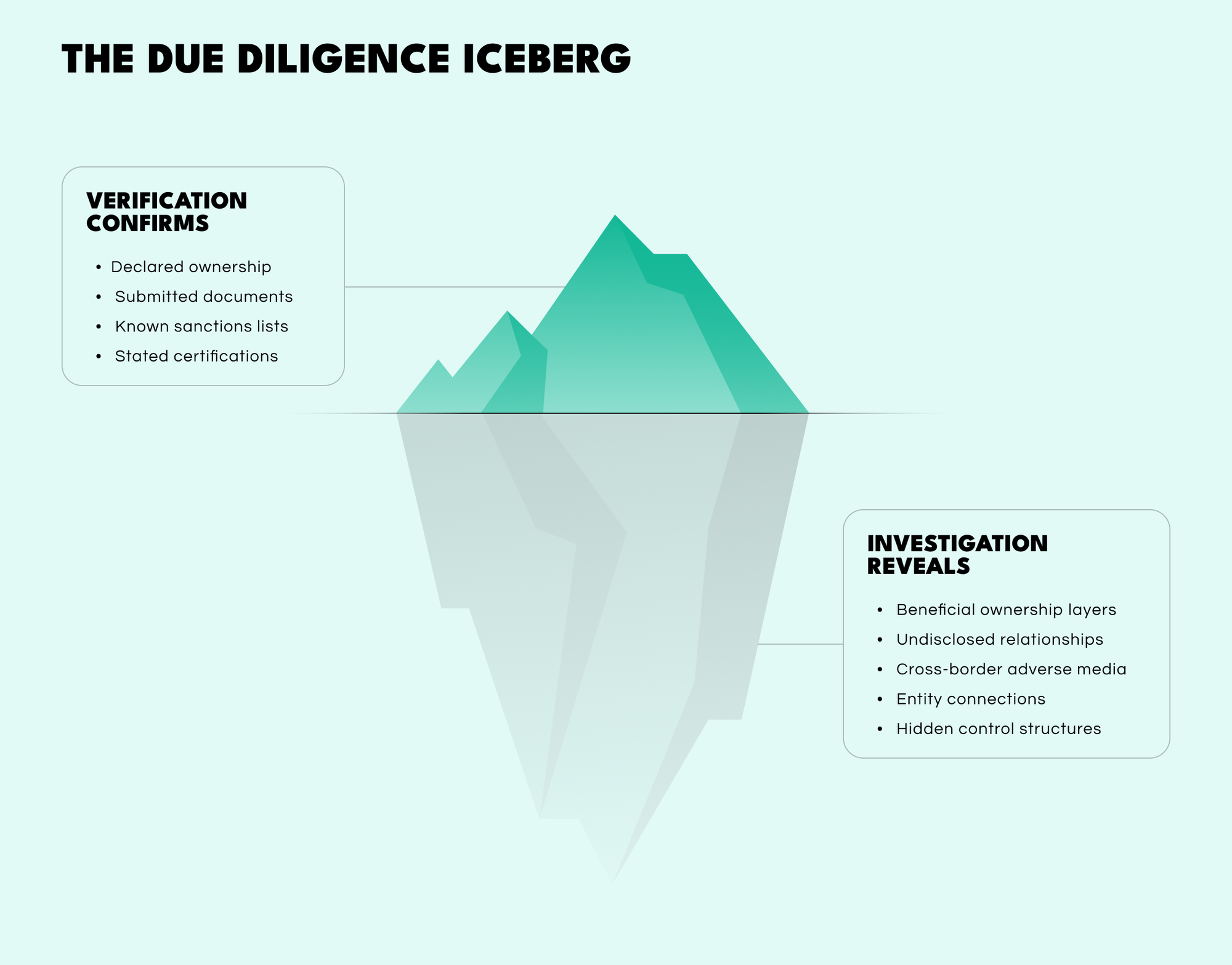

Most due diligence programs are built around verification. They confirm that the information an entity has provided is internally consistent, that documentation is in order, and that known sanctions lists have been checked. Verification is necessary. It is not sufficient.

The gap between what verification confirms and what investigation reveals is where the most significant risks tend to sit. Verification tells an organization what has been declared. Investigation determines whether those declarations reflect reality.

Above the surface, verification confirms declared ownership, submitted documents, known sanctions exposure, and stated certifications. Below it, investigation surfaces beneficial ownership layers, undisclosed relationships, cross-border adverse media, entity connections, and hidden control structures that counterparties would never voluntarily disclose.

For most of its history as a business practice, due diligence was primarily a financial and legal function. Teams reviewed financial statements, audited contracts, assessed liabilities, and confirmed regulatory status. The scope was defined largely by what the counterparty disclosed, and the process was confirmatory rather than investigative.

Several developments have changed that model significantly.

The complexity of ownership structures has increased substantially. Beneficial ownership layers, holding company networks, nominee arrangements, and cross-border structures make it genuinely difficult to determine who controls an entity through documentation review alone. A company may present a clear corporate structure that conceals real ownership several layers back.

The regulatory perimeter has expanded. Due diligence obligations are no longer primarily triggered by transactions. Anti-money laundering frameworks require ongoing customer due diligence. Sanctions regimes require continuous screening. Supply chain legislation now requires organizations to investigate human rights and environmental conditions across entire value chains. The EU's Corporate Sustainability Due Diligence Directive, which entered into force in 2024, extends mandatory due diligence obligations across entire value chains for large companies operating in the EU, with penalties reaching up to 5% of global annual turnover for non-compliance.

The speed and sophistication of fraud has accelerated with AI. Synthetic identities, AI-generated documentation, and deepfake personas have made surface-level verification significantly less reliable. A counterparty that passes standard document checks may not be what it appears to be.

83% of private equity leaders say their current due diligence approach has substantial room for improvement, a recognition that reflects both the increasing complexity of what needs to be examined and the growing consequences of getting it wrong.

Due diligence is not a single activity. Different decisions and different risk profiles call for different investigative approaches, and mature programs combine several of these simultaneously.

Financial due diligence examines an entity's financial health, accounting accuracy, revenue quality, debt exposure, and forward-looking financial risk. This is the most established form and remains central to M&A and investment decisions.

Legal due diligence covers contracts, litigation exposure, regulatory compliance, intellectual property, and any legal obligations that could create liability for the acquiring or partnering organization.

Beneficial ownership and corporate structure analysis investigates who actually controls an entity, tracing ownership through corporate registries, public filings, and open-source sources to identify the real individuals behind declared structures.

Reputational and adverse media review surfaces what official records often do not. Fraud allegations, regulatory actions, corruption concerns, and operational complaints frequently appear in public reporting long before they surface in formal enforcement databases.

Third-party and vendor due diligence examines the organizations an entity works with, depends on, or is structurally connected to. Direct vendor reviews address the most visible layer. The harder problem is what sits behind them.

Cyber due diligence has become increasingly important, particularly in M&A and technology partnerships, assessing an entity's security posture, breach history, vulnerability exposure, and data handling practices.

ESG due diligence examines environmental, social, and governance factors, now carrying regulatory weight under frameworks like the CSDDD that extend obligations deep into supply chains.

Enhanced due diligence applies a deeper investigative standard to high-risk relationships, triggered by factors including sanctions proximity, beneficial ownership complexity, politically exposed persons, or reputational red flags that standard review surfaces but cannot resolve.

Due diligence obligations have expanded in scope and depth across multiple frameworks simultaneously, and the direction of travel is clear.

The EU's CSDDD requires large organizations to conduct due diligence not just on direct counterparties but across their entire value chain, including subsidiaries, suppliers, and business partners. The obligation extends to identifying, assessing, preventing, and mitigating adverse human rights and environmental impacts. This is substantively different from traditional due diligence: it requires ongoing investigation of conditions that may be entirely outside an organization's direct control. Compliance begins phasing in from 2028, but organizations in scope need to be building programs now.

Anti-money laundering frameworks have moved toward continuous, risk-based monitoring rather than periodic review. The expectation is not that organizations conduct due diligence at onboarding and periodically thereafter, but that they maintain current understanding of their counterparties' risk profile as it changes.

Sanctions regimes have expanded in reach and complexity. Identifying direct exposure to sanctioned entities is no longer sufficient. Organizations are expected to identify indirect exposure through ownership structures, correspondent relationships, and connected parties, which requires the kind of network-level investigation that checklist-based due diligence cannot perform.

The practical implication is that organizations which built their due diligence programs around periodic review, questionnaire completion, and database screening are operating below the standard these frameworks increasingly expect.

Most effective due diligence programs move through a similar logical sequence, though the depth applied at each stage varies with the risk profile of the decision being made.

Investigations begin by defining scope: what decision is being made, which entities are involved, what level of risk is acceptable, and what time and resources are available. Without clear scoping, reviews either miss important issues or waste resources on irrelevant ones.

Evidence gathering expands from structured databases into open-source intelligence, public records, corporate registries, adverse media, and investigative sources. This is where the process moves from confirming declarations to testing them against independent evidence.

Analysis connects individual findings into a coherent picture. Ownership structures are mapped. Entity relationships are traced. Inconsistencies between declared and observable information are identified and assessed. This stage determines whether the review remains procedural or becomes genuinely investigative.

Risk assessment converts findings into a structured view of what the relationship actually entails: financial exposure, legal and regulatory risk, reputational concerns, operational dependencies, and any unresolved questions that warrant escalation.

Documentation records not just conclusions but the investigation behind them. Increasingly, regulators and counterparties require organizations to demonstrate that their process was substantive rather than performative.

Programs that perform most effectively share several characteristics that distinguish them from traditional verification-focused approaches.

Ongoing function rather than point-in-time exercise. Risk changes. Ownership structures change. Regulatory status changes. A counterparty that presented no significant risk at onboarding may present significant risk eighteen months later, and nothing in a questionnaire-based process surfaces that change until the next scheduled review.

Connected investigative capability. Standard screening and document review establishes the baseline. OSINT investigation and network analysis fills in the picture that baseline review cannot provide. These are not competing approaches but complementary layers that need to be designed to work together.

Defined escalation thresholds. Not every relationship carries the same risk profile and not every relationship warrants the same investigative depth. Effective programs define clearly what risk indicators trigger deeper investigation rather than relying on individual reviewer judgment under deadline pressure.

Documented process behind conclusions. Increasingly, regulators and counterparties require organizations to demonstrate not just that they conducted due diligence but that the process was substantive. An investigation that cannot be explained and evidenced is difficult to defend when scrutinized.

Due diligence has moved well beyond its origins as a financial and legal confirmation exercise. Modern due diligence is an investigative function that combines document verification, beneficial ownership analysis, adverse media review, network mapping, and continuous monitoring to determine whether what an entity represents about itself reflects reality.

The regulatory frameworks now driving due diligence obligations, from CSDDD to AML requirements to expanded sanctions regimes, reflect a clear direction: the standard is rising, the scope is broadening, and the expectation of continuous rather than periodic oversight is becoming the norm rather than the exception.

Organizations that continue to treat due diligence as a checklist activity will consistently miss the risks that operate outside what counterparties choose to disclose. Those that invest in the investigative layer connecting verification to genuine inquiry are better positioned to identify those risks before they become losses, regulatory findings, or reputational events.

Due diligence is the process of investigating a counterparty before committing to a significant decision. The standard has changed because regulatory frameworks including CSDDD, AML obligations, and expanded sanctions regimes now require organizations to investigate across entire value chains continuously rather than periodically at onboarding.

The main types include financial, legal, beneficial ownership, reputational and adverse media, third-party and vendor, cyber, ESG, and enhanced due diligence. Different decisions and risk profiles call for different combinations of these approaches.

The CSDDD requires large EU and non-EU companies to identify, assess, prevent, and mitigate adverse human rights and environmental impacts across their entire value chain, including subsidiaries, suppliers, and business partners. Penalties for non-compliance can reach 5% of global annual turnover.

Enhanced due diligence applies a deeper investigative standard to high-risk relationships. Common triggers include sanctions proximity, complex beneficial ownership structures, politically exposed persons, adverse media findings, or significant inconsistencies between declared and observable information.

AI has made synthetic identities, generated documentation, and deepfake personas more accessible and convincing, reducing the reliability of surface-level verification. Effective due diligence programs now need to test declarations against independent evidence rather than relying on document review alone.

Want to see how OSINT supports due diligence programs in practice? Book a personalized demo with one of our specialists and discover how SL Crimewall helps analysts verify beneficial ownership, surface adverse media, map entity networks, and build the investigative picture behind complex due diligence cases.